Weekly Report August 20

For new readers of the blog, I recommend reading the terminology page before the weekly reports.

I’ve been terribly busy preparing my move to Hong Kong due next Sunday and so that’s why the weekly report is late.

Stocks

Last week we saw a minor dip in stocks which does not count as a daily cycle low by any measures other than breaking the daily cycle up trendline and so I would classify that dip as a HCL. What comes to the bigger picture; the intermediate degree cycle being on week 28, we are due for an intermediate degree correction. The cycle which ended to the February crash lasted for 24 weeks. We could potentially see a similar crash event soon and with the S&P near all time highs, a likely scenario in my mind is that we’ll see a false breakout to new all time highs which acts as a perfect exit for smart money before an intermediate decline.

We are getting into the timing band of another yearly routine as predictable as spring rain. Perma bears calling for a crash in Autumn. Last year we heard the same calls for another October 1987 as we do every year but what ended up happening was that the S&P500 index rallied over 11% from late August until years end. What is different compared to last year is that we had an ICL in late August which reset sentiment and setup the stage for a rally for the Santa Claus rally and towards the January top.

A common misunderstanding is that the FED leads the market with its intrest rate decisions. This however has not been true since the 90s. After the 90s recession, central banks have turned from secrecy to transparency. As late as in the 80s, it was common for central banks to announce interest rate hikes without a warning and thus shock the markets. In the 90s, central banks understood that it’s better not to shock the markets than to shock them irregularly. Nowadays central banks publish detailed calendars for meeting and use forward guidance to inform the markets in advance. So, a serious stock market correction like a quick 10% crash to an ICL could derail FEDs rate hiking plans for September, but after seeing the action in the S&P last week, I think that we could have protection from the plunge protection team until the next FOMC meeting in late September.

If we would get an ICL which would come in form of a 10% crash lasting a week or two, it could force the FED to halt rising interest rates, which would in turn signal the markets that the FED is worried about the US economy. I think that if such events were to take place, we could transition into a bear market in stocks which would last until the 4 year cycle is due in 2020 or late 2019. In that case, commodities should rocket higher and oil would complete the 100% YoY rise which would push the US into a recession. For now, I think that it is likely that we will see a recession in the US in the next two years but whether it’ll start this year or the next depends on the FEDs actions.

As a recap, one should keep in mind that we are approaching the timing band for an intermediate degree correction in stocks and so I think that stops for long trades should be kept close. The next real buying opportunity (the ICL) is still ahead and so I wouldn’t push stocks too hard for now. If you have large positions in US stocks, I would personally hedge those as soon as possible.

Gold

If the FED would halt their rate hiking cycle in September, that would come as a big shock for the whole world. I think that gold would perform well under such circumstances but taken that I do not think that stocks are allowed to make a severe enough correction before the FOMC meeting, the odds for a rate hike remain high for now. We are definitely due for an intermediate cycle low in gold and so contrary to the stock market the cycle forces are trying to push gold higher. This has been the longest intermediate cycle as far as I know and definitely the longest in the 21st century.

As I wrote in the August Economic Outlook published on Saturday, I think that we should soon find out whether or not the Yuan gold peg is for real or nonsense. If it is for real and here to stay, it would align well with the US having a recession soon. The FED is going to push the US into a recession at some point as they always do no matter what. If they halt rate hikes in September, the odds are good that the recession will hit inside a year from now which could potentially lead to some nasty outcomes for the Dollar. I encourage everyone to read my latest Economic Outlook, to get a grip on what is happening in the world’s monetary sphere. The east is preparing for the end game whilst the west can’t seem to look beyond their feet.

Currencies

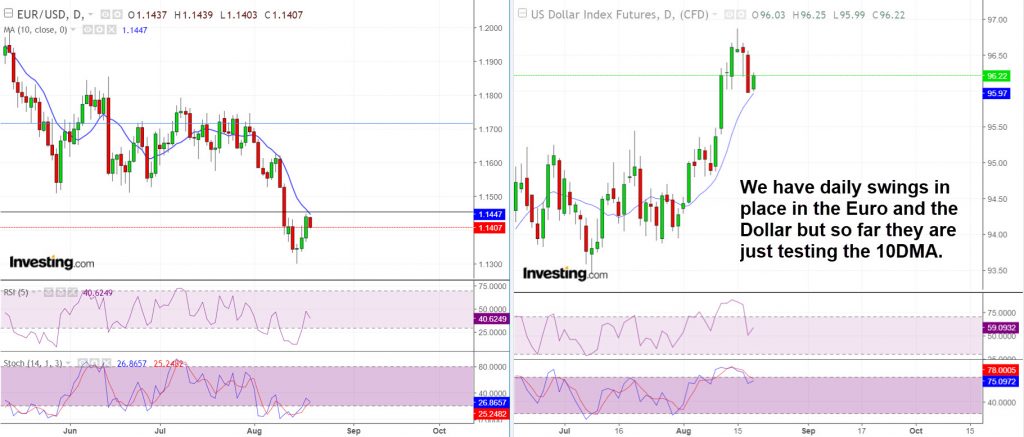

We had a daily swing low in the Euro and a daily swing high in the Dollar coupled with a weekly exhaustion candle in the Dollar and a bullish hammer in the Euro which could easily lead to weekly swings. I rarely consider fundamentals to be valuable in currencies, but as long as the US keeps rising tariffs and the FED is signaling pure fait on the US economy, I think that the Dollar will remain elevated against other currencies.

Why do I consider fundamentals to be mainly worthless in currencies? Take a look the Dollar index in the early 200s. The US experienced a massive boom from 2001 to late 2007, yet the Dollar weakened year after year. If the US was booming, shouldn’t money have flowed into the Dollar and not out?

The currency cycles have become quite irrational as the Dollar should have topped naturally many weeks ago. While it’s possible that the Dollar topped last week, I would remain cautious because if the US rises the tariffs on China, the Yuan is likely to plummet causing more turmoil to the emerging markets and pushing the Dollar higher. If the FED is going to halt rising interest rates, I think that the Dollar index will top at that point latest. The big picture remains the same as the Dollar is in a bear market and in my opinion, there is no way for the Dollar to go anywhere near the 2017 highs. I think that the 3 year cycle in the Dollar bottomed in February and the current rally is a result of that. The 3 year cycle will likely left translate and deliver a lower low next year.

The short term picture is a bit fuzzy but at some point the Dollar will have to deliver a DCL which should break the daily cycle up trendline and push oscillators to oversold at least.

What comes to the intermediate cycle, the Dollar is also due for an ICL which should break the intermediate cycle up trendline and push the weekly oscillators to oversold conditions. The current rally could turn out to be a false breakout of the multi week consolidation and the top for the intermediate cycle as well as the 3 year cycle, but for now the cycle count is too hazard for me to make definite calls for currencies.

To receive instant notifications on new posts, follow SKAL Capital on Twitter.