Economic Outlook August 2018

There are troubles in the air concerning the current status of the world’s economy. Trade wars, slowing global growth and the start of the quantative tightening (QT) era to name a few. From cycles analysis perspective, we are due for a larger four year cycle low in US stock market in 2020. This is just a rough estimate and we could see the bottom even sooner, as the current cycle is progressing towards the latter part of the 4 year cycle. In this post, I want to discuss my views of where the world is heading in the near term future.

Typical measures investors take in preparation for a bear market are moving allocation towards consumer staples or towards safe haven assets like bonds, gold or the US dollar. I am personally reducing my long term stock exposure and so not just reallocating. Currently the problem with bonds is that the ones considered as safe haven assets are barely yielding at all. In Europe, the German 30 year bund is yielding less than one percent as of 17th of August 2018 (Source: Bloomberg). This means that with inflation in Germany being at two percent (Source: Trading Economics), the real yield before tax is a negative one percent. The same issue is in many of the US bonds and notes as they are yielding in real terms close to zero percent before tax and after tax the yields are mostly negative.

With yields in many asset classes at historic lows, many investors have resulted to leveraging their portfolios to increase return on equity. This a good concept for a low interest rate environment, but when everyone is leveraging their investments the market becomes more unstable. We saw a prime example of this in the US housing crisis. In many parts of the world, we are exhibiting the same behavior as in the US before the housing bubble popped. This is partly because real estate prices in Europe and Asia hardly budged during 2008 and 2009. Many novice real estate investors hardly acknowledge this fact when they have a portfolio consisting of 10 apartments with 10:1 leverage. I know many of such people in Europe. With bonds yielding negative real interest rates for 10 years in a row, stock market valuations at bubble territory and real estate prices at or higher than in 2008, I consider the current debt bubble as the biggest bubble in the history of mankind.

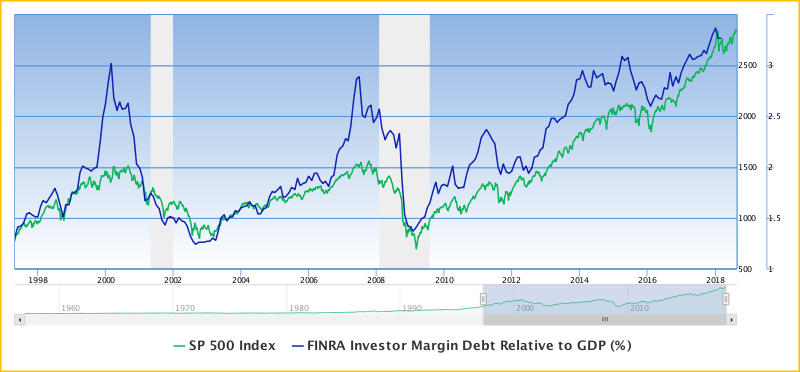

A good example of overleverage is margin debt, which measures how much leverage brokers are lending to their clients. As we can see from the chart below, margin debt to US GDP is at all time highs, which suggests that the stock market is more leveraged than it has ever been. All of that debt will come out all at once during a major sell off like a bear market.

Source: Gurufocus.com

Now that the central banks around the world have multiplied their balance sheets and rates have been kept at historic lows for a decade, what are the options left once there is another recession or a financial crisis? What will happen when everyone with their overleveraged portfolios try to exit the market in a 2008 type of sell off? Debt and overleveraging were a major cause of the 2008 market crash and now that the problem is even bigger. Debt and overleverage will once again be a major component in the next bear market in stocks. When this happens, the FED will be forced to cut interest rates and after rates are at zero the FED will have to do QE4. I believe that once the FED resolves to QE4 the FED will permanently destroy the reserve currency status of the modern US dollar. I do not think that the collapse is imminent, but from the cycles analysis perspective, I give odds of above 50% for this to happen in the next two years.

Gold

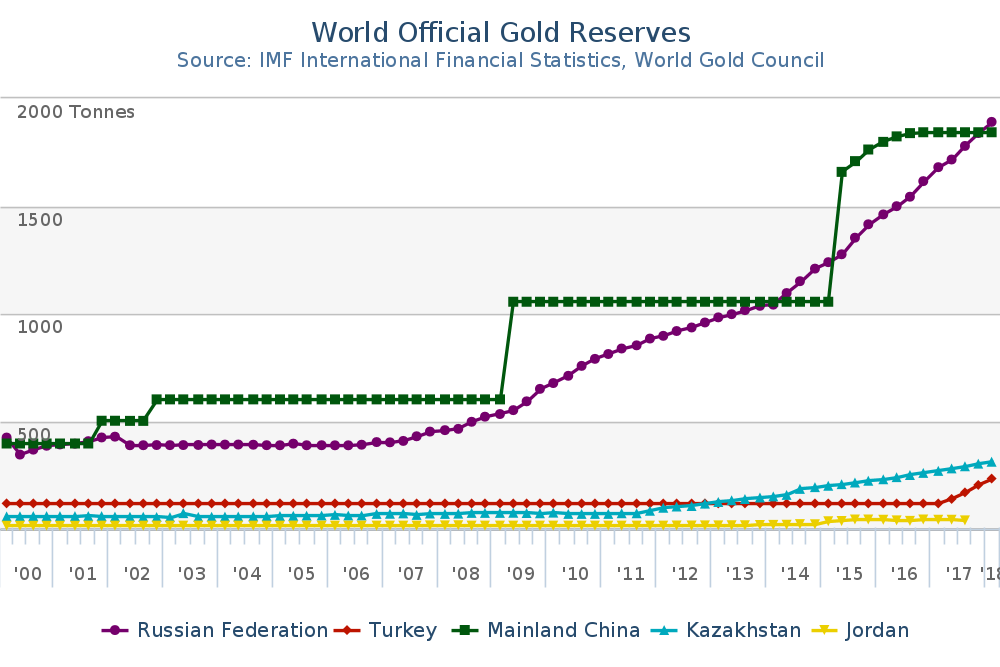

An interesting fact has been gaining more attention in the past few years. Many of the large countries in Asia have been accumulating large physical gold reserves. As we can see from the chart below, China and Russia have both been accumulating physical gold since 2008 and lately Kazakhstan and Turkey amongst others have started to accumulate reserves as well.

Source: World Gold Council

What strikes out, is that China claims to have increased their reserves between Q1 2015 and Q2 2015 by over 600 tonnes. With global gold mining output being approximately 2500 to 3000 tonnes per year (Source: World Gold Council), something seems fishy. After the jump in reserves, China continued to accumulate quarterly for 5 quarters, but suddenly went back to flat in Q3 of 2016. Really.

In other words, I do not place much faith in the economic figures from the Chinese government. Hong Kong import figures and China’s gold mining industry output are suggesting that much more gold has been flowing into China for a long time already. The evidence is suggesting that China holds much larger reserves than what they officially claim. (Source: Bullionstar.com)

During a conversation about the topic with a senior analyst, he asked me “China can print as many Yuan as they want. If you have a printing press what difference does it make what the price is of anything? And what use would they have for all this gold? Let’s face it no one is willingly going to back their currency anymore and limit their ability to print money.”

I see the first question as partially self-fulfilling. First of all, the fact that central banks can indeed print as much currency as they want and thus increase their money supply, creates the dilemma of inflation control. In the current world, central banks need to keep printing currency in order for the whole system to function. Governments need to create inflation so that they can borrow purchasing power of 100 units today, spend it and then in 30 years pay back 55 units of purchasing power which is the result of two percent inflation in 30 years.

One of the main purposes of a central bank is price stability, which has later been defined by many as about two percent annual inflation. Such a Ponzi scheme cannot go on forever. Extensive printing of fiat currency has always led to destruction of that currency and in many occasions this has happened via hyperinflation. History has proven this numerously, with Venezuela, Iran and Turkey being latest of the long list of destruction via inflation.

Noted that the same analyst has also hypothesized that by suppressing the price of gold, oil, copper and other commodities, central banks are able to control overall inflation. If the price of raw materials, inflation hedges and commodities in general are kept in check, that solves the inflation issue in the producers end. However, inflation consists of many other aspects as well like real estate prices, services and wage inflation. Many of which have nothing to do with commodities.

Another issue with controlling inflation via the futures market is that demand in other countries might spike due to a natural disaster, an epidemic or just poor weather conditions. This could leads to rising prices, much like we are seeing in milling wheat futures lately. Prices could rise, if not in the suppressed futures market, but in the actual spot market. In other words, inflationary pressures can come from uncontrollable sources.

I have a lot of respect towards this analyst and so this is just my take on the topic. I would not be the person I am without his guidance and this site would not exist in the current format without him.

The second question “What use would they have for all this gold?” is a matter of defining the purpose of holding gold in a central bank.

The answer lies in the balance sheets of major central banks. ECB, FED, Deutsche Bundesbank, Bank of France, Bank of Japan et cetera, have all thousands of tonnes of gold in reserves. Even the central bank of central banks, the International Monetary Fund has close to three thousand tonnes of gold in their reserves.

In Keynesian economics, gold is seen as a commodity with no monetary use. Universities around the world see Keynesianism as the proper approach to economic issues. With central banks exhibiting Keynesian economics, why would a central bank be holding such gold reserves if gold was just a commodity and not a monetary asset? Central banks hold reserves in Dollars, Euros, Yuan and other currencies as well as in gold. Central banks do not hold platinum, silver or any other metals, much less other commodities, but they are the single biggest holders of gold non the less. If gold has no monetary use, why do not central banks just dump it to the market? If you have a printing press, you should not care if you make losses while dumping gold as you can shrug those off those losses by printing more currency. The answer is that gold plays a major role in our current monetary system.

A point can be made, why would any country go back to sound money once fiat has been widely accepted around the world? Because that is the way to win the game.

It is a well known fact that the Chinese want to become the greatest economy in the world. To achieve this objective, they need to claim the reserve currency status. This is the way the British empire claimed their power in the 19th century and how the US did it in the 20th century after world war two. Control the reserve currency, control the world’s economy.

With the global economy seen slowing and possibly falling into a recession soon, central banks will be forced to resolve back to easing their policies. China realizes that it is not going to win a printing war with the US as there are no winners in that race and so they can never outnumber the dollar without crashing their own currency in the process.

The Chinese also understand that if the dollar loses its value due to a currency crisis, much like we are seeing in some emerging markets, that no fiat currency will remain reliable. All fiat currencies ultimately fail. As a French author from the 18th century called Voltaire put it: At the end fiat money returns to its inner value—zero.

China needs to do something differently in order to regain their glory as a global power as they were during the previous peak of the east west cycle 250 years ago. What China could do is to change the rules of the game by bringing gold back to the monetary table as a stabilizing component. For the past 3000 years the solution for a collapsing fiat currency has been gold. We have to remember that China is a forward thinking country and currently one of the few countries in the world to publish a 5 year plan. Currently most western countries only look at the next quarter or the next year at most.

Russia acknowledges the fact that they cannot rival with the Chinese economy and so it is better to play along with a rising giant than a dying one.

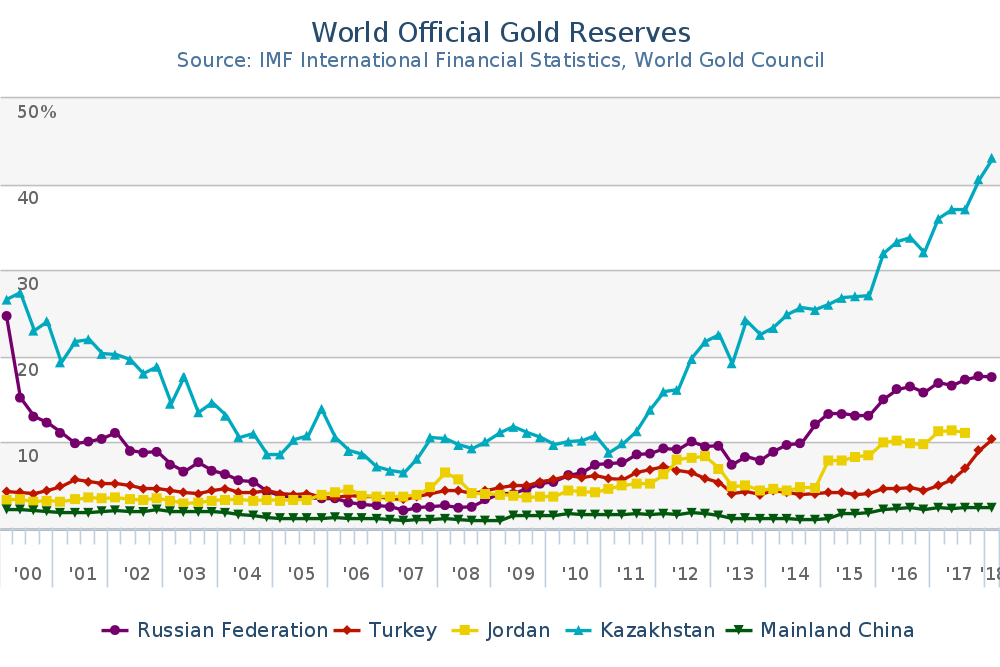

Eastern countries which do a lot of trade with China and Russia have noticed that the two eastern super powers have been piling into gold. Kazakhstan, Turkey, Mongolia and many other strategic trade partners of the two are also converting their reserves into gold. It could even be that these countries have been noted by Russia or China about their plans.

Kazakhstan is a prime example as they currently hold over 40% of their exchange reserves in gold. Kazakhstan is building the good old “Keynesian gold cage” around itself. With the what is going on in the east, it is well foreseeable to say that major changes are taking place.

Source: World Gold Council

It is likely that the Chinese central bank or in other words the People’s Bank of China (PBOC) is letting Yuan devalue in order to diminish the impacts of the US tariffs. After the US placed 10% tariffs for many Chinese goods, the Yuan has weakened against the dollar by close to 10%. For now, it seems that if China and the US cannot find a solution quickly, the US will increase their tariffs to 25% in early September. These tariffs will lead to slowing consumption and economic growth and so the global recession aspect gains some votes.

The Yuan Dollar crossrate has been highly correlated with the Dollar gold crossrate for the past two years and in the past 10 months the correlation has become even tighter. Although correlations emerge and break all the time in the markets, there is an interesting theory behind the Yuan gold correlation which is supported by many factors.

As China keeps hoarding gold monthly, a Yuan devaluation makes these gold purchases costlier to perform. In order to devalue Yuan and simultaneously buy lots of gold affordably, you need to lower the price of gold in dollars. This means that you would need to manipulate the price of gold down so that the devaluation would not affect your purchasing power.

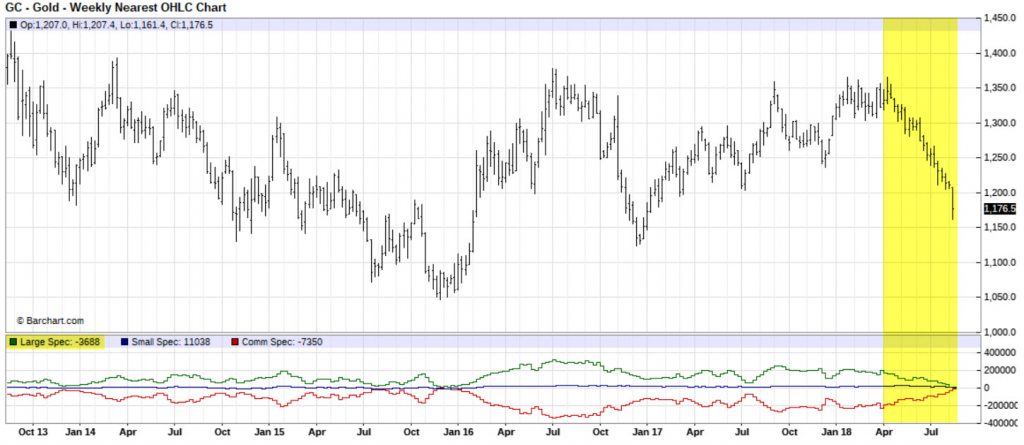

China is able to participate in the futures markets via their sovereign wealth fund. If China were to operate in the futures markets via this fund, that participation would show up in the Commitment of Traders report as large speculators. As we can see from the chart below, large speculators have been loading up shorts throughout the whole decline.

Source: Barcharts.com

Just as a point of reference, last time large speculators were net short gold was in August 2002 and even then they were net short for just one week. So, this is not something you see every year but maybe once a decade.

The Chinese sovereign wealth fund has close to trillion dollars in assets under management and whilst there is no way to prove that China is behind the large speculators number, manipulating a few billion dollar gold market via margin would certainly be a “no biggie”.

In the past few days the correlation between Yuan and gold has been disrupted as gold has been falling in Dollars whilst the Yuan has been resisting the decline. So, has the correlation broken and the theory completely scrapped? Not necessarily.

Question. How would you construct an algorithm that is designed to keep up your purchasing power whilst your currency devalues if you would have close to unlimited resources? Surely you would make the algorithm sell commodity futures as your currency falls, but would you make the algorithm buy if your currency was to rise? Probably not, because if the price of the commodity falls naturally while your currency rises, your purchasing power goes up naturally. This is probably okay for China. So, China sells if gold tries to go up as well as when Yuan devalues, but they will not buy if gold falls naturally.

What comes to the “China can just print more money and so price does not matter” argument, China does not want to flood the markets with fiat Yuan if their goal is to keep the trust of the investors. China is very strict when it comes to the Yuan and that is partially why they have separated offshore and onshore Yuan.

There were not a lot of dollars circulating around the world before the world wars. Countries in war at Europe paid for their US made equipment with gold and so gold flowed throughout the wars from Europe into US. By controlling the worlds gold reserves, the US was able peg the Dollar into gold after the wars and start flooding the world with strong gold backed currency, which they later on have been devaluing via inflation. This just goes to show, that a reserve currency status is achieved by making your own currency desirable but not necessarily easily accessible.

The big picture is as follows.

The global economy along with the US tumbles into a recession at some point. This leads to central banks around the world to quit QT and resolve back to QE. I suspect that as that happens, we are going to see a global currency crisis as inflation picks up dramatically all over the world. At some point the Chinese president Xi Jinping amongst other leaders of China decide that China has accumulated enough gold and that the environment is suitable to announce a new gold standard. This would be a major plea of distrust to fiat currencies from China and is probably the worst nightmare of western central banks. China could go to the extent to say that they will not do trade in anything else but Yuan and gold, without a special trade deals like the ones they are working on with Russia.

The Canadian government sold all of its gold back in 2016 (Source: CBC) and so they amongst many other countries would have to buy lots of gold to keep up the trade with China. I do not think that Canada or frankly any western country would be able to get along without Chinese products. By resolving to a gold standard, China would force everyone to buy gold. Gold being a very thin market, prices would have to sky rocket due to increased demand. With China and Russia holding potentially more gold than any other country, this would lead to a massive wealth transfer from west to east. By the way, the US gold reserves have not been counted since 1953 (Source: Bloomberg) so do not take it for granted that the gold is still really there. The best way to prop up a country from a recession is to get fresh investments into the country so that you get money flowing again. This would be achieved by making Yuan and gold desirable for every nation in the world. China is hoarding gold for the end game, whether that is next year or still 20 years away.

My conclusion is that the western world is collapsing to under its own weigh and that the east will be the true winner of the next global recession.

If you can provide me a reasonable explanation of why China, Russia and other eastern countries have been accumulating gold for other than in preparation for a major economic and monetary shift reasons, please reach to me via Twitter or LinkedIn.

To receive instant notifications on new posts, follow SKAL Capital on Twitter.