Weekly Report September 9

For new readers of the blog, I recommend reading the terminology page before the weekly reports.

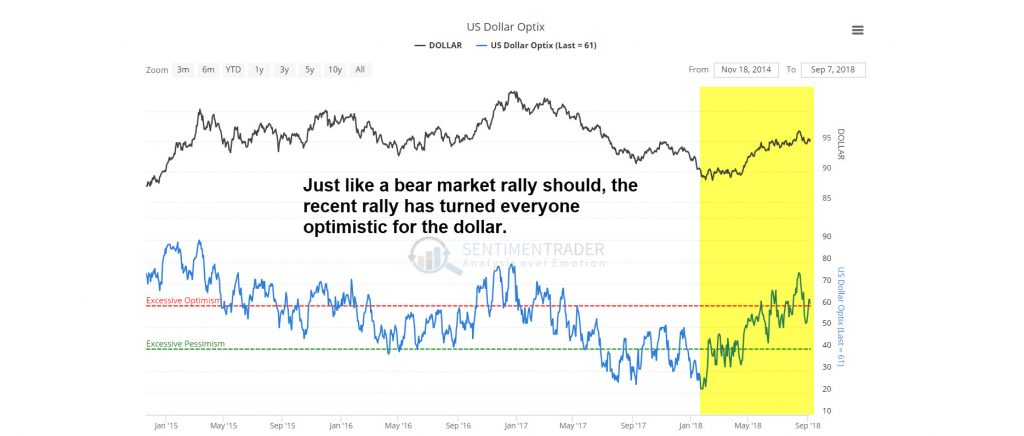

Currencies

The euro and the dollar have progressed the way I suspected in the previous weekly report. The euro fell lower towards what I believe is a HCL and the dollar rallied as the result of that. It’s still a bit unclear to me whether the dollar has completed a DCL since the daily cycle trendline hasn’t been broken and so it could be that the dollar drops to a true DCL in the coming two weeks and produces another bounce which pushes the euro to its DCL in early October. The most likely outcome for now is that the dollar will resume the downtrend next week which will confirm the HCL in the euro and we’ll be able to construct a healthy daily cycle uptrend line for the euro. I also believe that the dollar has begun an intermediate decline which should break the intermediate cycle uptrend line. I believe that the euro will make significantly higher highs during the next intermediate advance.

People are still bullish for the dollar and bearish for the euro due to how the past intermediate cycles advanced. I’ll say it again. The dollar is in a bear market which means that the dollar is going to make lower lows later this year or early next year. This has been a perfectly normal bear market rally for the dollar, which has done exactly what it’s supposed to – turn everyone bullish to fuel the next leg up.

Source: Sentimentrader.com

The non-farm payrolls triggered a bounce in the dollar but if I’m correct and the euro did complete a HCL on Tuesday we should negate this early next week. Same applies to other markets which corrected as a result of the jobs report on Friday. If we look at the dollar from a fundamental perspective – which I don’t really like to do as I don’t think that currencies have any fundamentals but let’s play with the idea – the dollar has been pricing in strength in the US economy relative to the rest of the world for the past 7 or 8 months. With the dollar lacking momentum in the past three months, it seems as if the dollar has already priced in strong economic figures and policies for at least the rest of the year. This means that positive surprises shouldn’t result into large leaps up, but negative surprises could result into big moves down. There is potentially one huge negative surprise coming later this month which I’ll discuss in the stocks paragraph below.

Gold

As in the euro, I believe that gold produced a HCL on Tuesday and so we should get traction to the upside and make some higher highs next week. The 3 day RSI on gold did reach oversold which is typical for HCLs. The jobs report on Friday did shuffle the pack a bit in gold as well and so to play safe one could wait for another daily swing low in gold to enter. Next week should tell us whether I’m wrong or right with the HCL.

For gold, the intermediate correction is probably already over as I suspect that the DCL printed on 16th of August will turn out to be the final intermediate cycle low as well as a yearly cycle low. Gold and silver don’t have to bottom at the same time as we saw in December 2015. Silver actually bottomed two weeks after gold in the 2015 bear market bottom after which silver rallied over 50%. The bear market bottom was not easy nor pretty but it led to spectacular gains in the next six months, I suspect that we are setting up for something very similar and if we are to break out above the 2016 highs, then the current prices will not be visited for decades. As we saw in the 2015 bottom, the actual bottom was followed by four weeks of churning sideways but the reward was well worth the pain.

Oil

We printed a nice reversal candle on Friday and I suspect that’ll mark the low of the HCL in oil. As I mentioned in the previous weekly report, I was expecting gold, oil and the euro to drop into half cycle lows which I think has now played out. Oil and commodities are probably starting new intermediate cycles which should rally for several weeks to come. I suspect that if oil is able to break above its July highs soon, that could trigger a vertical climb in oil prices as traders would turn back to thinking that the oil market is bullet proof. We need to get to new highs quickly though since we shouldn’t be wasting too many days of this first daily cycle. Breakouts are usually more sustainable when they come early in intermediate advances compared to when they come late in the intermediate cycle as I’ll show you in the stocks paragraph below.

The CRB did also correct this week and so I think that commodities in general have also moved to a HCL alongside with the euro. Many of the commodities have been stuck below their 10 day moving averages and so I’m wondering if there’s pressure building up for the next leg up.

I did buy a couple more CL February calls with a strike price at 75 USD on Friday though I bought them before the dip to Fridays intraday lows and so I could have got a better bang for the buck so to speak. Then again, the calls have lots of time on them and so there’s no need to worry about intraday wiggles if we are to transition into an energy bubble preceding a US recession.

Stocks

Stocks seem to be working their way to a DCL which should be due in the next two weeks. 30 weeks into an intermediate cycle stocks are also overdue for an ICL which could play out as a scary selloff over the next two to four weeks. As I mentioned in the oil paragraph above, breakouts that occur late in the intermediate cycle are usually not sustainable. This is exactly what we’re seeing in stocks as the S&P500 has effectively negated the breakout to new all time highs and even closed the week below the 2900 round number. Breakouts like these are often fakeouts which get retail traders buying and offer the smart money a perfect exit for their positions.

Now here’s where it gets really interesting. With 30 weeks into an intermediate cycle we are overdue for an ICL in stocks. If we can manage to get a true ICL before the supposed FED rate hike later this month, the FED could actually step back from the rate hike. For now, Powell seems to play tough ball with Trump who has reportedly said that his not that happy with the FED rate hiking policy but as Peter Schiff mentioned in one of his podcasts (Fed to Let The Inflation Genie out of the Bottle) the FED is slowly changing towards a more dovish tone. Currently the odds for a rate hike in September evaluated by the FED Funds futures stand at close to 100% (99,8% to be exact) and so we should see this probability fall dramatically over the next two weeks if the FED is going to step back on the rate hikes. There’s no chance in hell that the FED would skip a rate hike with FED Funds showing a 100% priced in rate hike. The days of central bank surprising the markets are long gone.

Currently I wouldn’t give this scenario more than a 30% chance of materializing, as I do think that the FED will once again prop up the stock market close to or to new all time highs by the time of the FOMC meeting. This gives the FED tailwind to push through the next rate hike. Needless to say, at this point a skip to raise rates would signal weakness in the FED and I’d say that the odds for a recession later this year would go way up. In case of a recession, Oil offers a good play.

To receive instant notifications on new posts, follow SKAL Capital on Twitter.