Weekly Report July 1

For new readers of the blog, I recommend reading the terminology page before the weekly reports.

Gold

As I’ve been saying for weeks now, the best opportunity on the market at the moment lies in the precious metals sector.

We saw a big up day in the miners on Friday and as the current intermediate cycle is mature, we tagged extreme pessimism in gold and we got a good volume up day in the miners on Friday plus a daily swing low in gold, silver and the miners, I’d now give very good odds that the YCL formed on Thursday. In order to get confirmation of that, we want to see an aggressive week in the metals next week. A weekly swing is the first indication of a completed ICL and if we close the week strong the odds are good for a completed YCL.

YCLs are the best time of the year to buy call options. To point out, I’ve carried on my plan of adding to the silver December call options position on every day silver makes a lower low. The position is at good size and a move to the 2016 top would produce gains upwards of 1 000%.

Currencies

There isn’t really anything new in the currencies either. As I mentioned in the June 10th Weekly Report, I believe that the dollar is in a long term bear market which should run well into the 2020s. The dollar has run a bit more than 8% during the last 19 weeks of its current intermediate advance, but for the last 5 weeks the dollar has struggled to make new highs. These kinds of moves are perfectly normal during a bear market. I pointed out in the June 10th weekly report that in the last bear market, the dollar once rallied 15% yet it still stayed in a bear market. I expect the dollar to form or to have already formed an intermediate degree top and I still think that the dollar will drop to new lows before the end of this year. We got a very bearish looking exhaustion candle on the DX weekly chart and so the intermediate top may have already formed. If the dollar starts to fall, this would be very bullish for gold which should start an aggressive move higher.

As the dollar falls, euro will strengthen. The euro has found good support at the 1,15 level and as of Friday we have a weekly swing low in place in the euro. This setup is similar to the setup in gold at the moment and a strong close next week would indicate that the euro has also put in its YCL, which is already way overdue.

Stocks

Stocks are acting the way I predicted in the last weeks weekly report. It’s still a bit fuzzy whether or not we completed a DCL this week. The bigger picture currently remains: We are getting mature in the intermediate cycle and so it’s getting riskier to stay long stocks. We might get another right translated daily cycle, but I wouldn’t bet the farm on that. I believe we will get an ICL in the next month or two depending on whether we get one more right translated daily cycle or not. I suspect that the next intermediate cycle will break stocks out of the 5 month long consolidation phase and the next ICL is the time I want to go long stocks again. At the moment the best opportunity still lies in precious metals and the miners, so stocks are a no go for me for now. If we can get a deeper dip to the DCL next week, I’ll consider a small long position for the short run.

Oil

Oil on the other hand had a very powerful week and recovered to new highs. The action is very similar to the move which the tech stocks experienced after the drop in February. As with stocks back in February, we now face two options. 1) We drop back and start forming a trading range like stock have been doing for the past 5 months. 2) We transition into a bubble, Saudi Aramco gets a great IPO and the US slips into a recession in 2019.

The second option would align with the bigger picture way better than the first option.

The economical big picture:

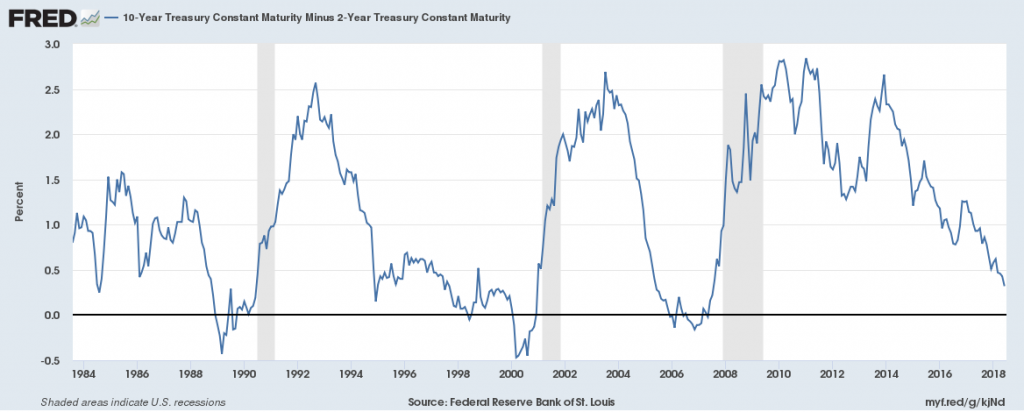

Stocks are closing in on their 4 year cycle low which is due in late 2019 to 2020. I examined this in a recent article named ‘What are cycles?‘. A year long bear market in stocks would be typical for a recession. The US yield curve is starting to flat out at a rapid rate. An inverted yield curve has been a good indication of an upcoming recession in the past as you can see from the picture below which represents the spread between the US 2 year note and the 10 year bond yields. An even better indication of an upcoming recession has been a 100% rise in oil prices in a year or less which I discussed in the previous weekly report. This has been nearly a foolproof indication since the 70s. So, you see a bubble in oil, the 4 year cycle low in stocks and an inverted yield curve would all fit the picture with each other. This would also fit in well with the longer term outlook I have for gold and silver. I think that gold will make new all time highs big time before end of this decade and the aftermath of the recession could potentially launch gold prices upwards of 5000 dollars per ounce before the next 8 year cycle low in gold is due between 2022 and 2024. Cycles tend to align with certain economical events like recessions and we are statistically due for a recession, but it’s harder to say when it’ll realize. I suspect that if we get a bubble in oil, we’ll see a recession before the end of this decade.

An inversion in the yield curve has been followed by a recession in the past and so it’s a valid indicator in my opinion. We are closing in on an inversion and if the FED keeps rising rates this year, I think we’ll see an inversion later this year.

To put things in order I say this again. I’m not preferring any trades currently besides the precious metals which I think will deliver massive gains in the next 2-4 months. If we get another strong week for oil, I might do an “explosion” position with oil call options. This means a very small position size, lots of time and deeply out of the money call options. Leverage in an explosion position is massive and so the risk must be managed with a small position size. I also do not prefer buying into overbought conditions and so the bet would be all or nothing as a decline to an ICL would be devastating for the options which in a trading range would never recover their value.

To receive instant notifications on new posts, follow SKAL Capital on Twitter.